Continuing its year-long celebration of its 75th Anniversary, Merritt & Harris, Inc. sponsored a gathering of its alumni and current employees on May 24, 2012 at Ryan Maguire’s Ale House in Manhattan’s Financial District. Manny P. Kratsios, President & CEO, welcomed those who once worked at M&H, thanking them for their contributions to the long-term success of the firm. Many of the “old-timers” now contribute the experience learned at M&H as employees of other construction consulting firms or with lending institutions. Mr. Kratsios asked those in attendance to share in a moment of prayer in remembrance of the firm’s past president, Buzz Harris, who passed away in 2011 and under whom many of the alumni learned the consulting business.

All posts by admin

The Top US Cities for New Home Construction

We encourage to check out this article on current trends in residential construction: http://www.citylab.com/housing/2012/05/top-us-cities-new-home-construction/1935/

Florida Office Gets New Manager

M&H President & CEO Manny Kratsios has announced the promotion of James Mako, P.E. to Senior Associate and his appointment as the new Branch Manager of the firm’s Deerfield Beach, Florida office. Mr. Mako holds a Bachelor of Science Degree in Electrical Engineering from Florida Atlantic University and is a registered Professional Engineer in Florida. Jim joined M&H in 2007 as Project Manager after closing his own firm. He has performed as the construction consultant on several significant M&H projects including the Dallas Cowboys Stadium and the Scrub Island Resort in Tortola, BWI. Mr. Mako succeeds Michael J. Dwyer, Principal, as the Florida Branch Manager. Mr. Dwyer has relocated to the firm’s New York City headquarters and will focus his efforts on the Cost & Review Group, which he has headed for many years.

M&H President & CEO Manny Kratsios has announced the promotion of James Mako, P.E. to Senior Associate and his appointment as the new Branch Manager of the firm’s Deerfield Beach, Florida office. Mr. Mako holds a Bachelor of Science Degree in Electrical Engineering from Florida Atlantic University and is a registered Professional Engineer in Florida. Jim joined M&H in 2007 as Project Manager after closing his own firm. He has performed as the construction consultant on several significant M&H projects including the Dallas Cowboys Stadium and the Scrub Island Resort in Tortola, BWI. Mr. Mako succeeds Michael J. Dwyer, Principal, as the Florida Branch Manager. Mr. Dwyer has relocated to the firm’s New York City headquarters and will focus his efforts on the Cost & Review Group, which he has headed for many years.

To contact Jim Mako at our Deerfield Beach, Florida office, please call 954.570.5559.

M&H Honors Company Veterans

Each year during the holiday season, it is customary for Merritt & Harris, Inc. to honor employees for their length of service to the firm in increments of 5 years. At the firm’s Holiday Party in New York and at a special luncheon for the honorees, Manny P. Kratsios, President & CEO, recognized Mary Anne Brennan, Proofreader, and Tom Richard, AIA, Principal, Director of Marketing and former President & CEO, for 30 years of service. He, also, honored William J. Doody, Principal and CFO, for 25 years of service; William McCallion, AIA, LEED AP, Manager of Quality Control & Training for 20 years with the firm; Joseph Marciano, PE, LEED AP, Senior Associate, for 15 years of service, and Michael Negron for 5 years as the Cost & Review Group’s Document Coordinator. Each honoree was presented with a certificate of appreciation and an American Express Gift Card appropriate to their tenure as a token of appreciation for their years of commitment to the firm. Merritt & Harris, Inc. is proud of the fact that 40% of its employees have been with the firm for 20 years or more.

On the Road to BIM and IPD

By William McCallion, AIA, LEED AP, Manager of Quality Control & Training

The emerging technology of BIM (Building Information Modeling) holds the prospect for a paradigm shift in the way buildings are designed and built. Enabled by the increasing availability of greater and cheaper computing power, Designers and Contractors are more empowered to record their visualizations to greater and greater degrees. BIM is one of the outcomes. Simply put, BIM is a virtual 3-D model of the building; however, it doesn’t stop there. In addition, there is, also, 4-D and 5-D, which is basically attaching information such as scheduling and costs to the model. (I think physicists might have a problem with that labeling.) Furthermore, other programs, such as daylight or energy studies, can plug into the model. The 3-D model is “smart.” Whereas in a 2-D environment, lines represent walls, in a BIM model those lines “know” they are walls. A wall that realizes that a window size has been changed, for example, can then direct the other related aspects of the model to change in kind. This is a significant advance.

With these tools, it is, in essence, possible to “build” an entire building virtually before a shovel goes into the ground, knowing its cost and schedule. One of the unique features of BIM is in the coordination of disciplines. Previously, the Designer of Record would be responsible for assuring that there are no conflicts between, let’s say, where a duct runs and where a beam runs, a tedious undertaking to say the least. BIM automatically presents such “crashes” to the Designer in real time, saving time and effort. Knowing virtually every aspect of the building prior to its construction has the possibility of eliminating unanticipated change orders, the bane of many a project’s budget. This information is usable throughout the life cycle of a building, particularly in the facility management cycle, in a way the drawings have not been.

However, the real shift is the way that the information gets into the model. When Brunelleschi won the competition for the Duomo in Florence, he was not only the Designer but also the Master Builder directing the construction of the building. In modern times, these tasks have been specialized, separating Architects from Contractors, with Architects disavowing responsibility for the means and methods of construction and Contractors disavowing any responsibility for design. A body of law and insurance policies has evolved to service this methodology. However, now that we have the technology to put information from both sides into one vehicle, a new relationship needs to evolve. The AIA (American Institute of Architects) has termed this relationship the Integrated Project Delivery (IPD) method. In essence, the Contractor (and in many cases a specialty subcontractor) joins the Architect during the design process providing information (such as cost and scheduling) for the model. The advantage is obvious, as the Architect can incorporate changes to the design based on the information the Contractor has provided. There is no need for “value engineering” at the end of the design process because it was done in real time during the design. The AIA has established new contracts to reflect this change; however, as this technology is still emerging, more will be revealed, and a body of law and insurance policies will need to evolve. And what might the future hold? One vision is that the model will be directly connected to fabrication facilities so that the model can order the components it needs when it needs them; we’ll see.

Finally – An Expert

by Tom Richard, AIA

A few years ago, in anticipation of an upcoming executive retreat, the facilitator distributed questionnaires to the would-be participants. One of the questions was, “What would you like to be known for in your industry?” I remember my response was, “I’d like to be known as an expert in something – anything.”

One day during my tenure as the President & CEO of Merritt & Harris, Inc., I received a phone call from a person purporting to be an employee of the BBC (British Broadcasting Corporation) radio. The person informed me that the talk show he represented was doing a segment on the law being proposed in Parliament that would prescribe minimum sizes for seating in sporting and entertainment venues. He had been referred to me as an expert in American stadium issues (Our M&H Sports Group had, at the time, served as consultants on more than 25 professional sports venues). The voice sounded suspiciously like one of my fellow principals affecting a phony British accent. Pulling a practical joke was certainly not beyond his idea of fun. Later I thought, “What if this was a legitimate call? I had better bone up on my seating history.” As the new Yankee Stadium was in construction at the time, I figured it was a good focus for discussion should the call turn out to be on the up and up.

At three o’clock that afternoon, I received a call informing me that the British program was on the air and that I was to stand by until addressed. (Wow, this really was a legitimate event.) When quizzed by the program’s hosts, I explained, “The original ‘House That Ruth Built’ had opened in 1923 with a capacity of 58,000 seats, some supposedly as narrow as 14 inches. The stadium capacity grew to 82,000 in 1928 when the grandstands were expanded and wooden bleachers were installed. The 1973 to 1976 renovation saw the old 18 inch wooden seats replaced by 22 inch wide plastic seats. The capacity was reduced to 54,028. In 2008 the new Yankee Stadium opened with 50,086 seat with widths ranging from 19 inches to 24 inches and leg room expanded by 3 ½ inches to 9 ½ inches, depending on the location. Judging from the expansion of the size of the seats, it can be deduced that American rear ends also grew, as did the length of their legs.” The response of the program hosts was that as long as Americans gorged themselves on chips (French fries) and hot dogs, our need for ever expanding seat widths would continue and the capacity of our existing venues would, therefore, continue to shrink.

So there you have it – I was finally an expert in something – and an international one at that. I never thought I would be deemed an expert in American rear end sizes, but now I apparently am. Be careful about what you wish for.

Cost Corner and Rental Apartment Construction Costs

by Michael J. Dwyer, Principal, Cost & Review Group Leader

New construction has not seen the recovery that was hoped for this year, but there is a bright spot emerging. Rental apartment buildings are anticipated in a number of larger cities, and the demand for these apartments is growing.

There are many indications that rental apartments will be in demand over the next three years as the housing crash has caused displaced homeowners to look for other living arrangements. The appeal of homeownership has, also, lost its luster, because of the “recession” and many would-be buyers are seeing rentals as a worthwhile option.

Although material prices have risen (generally 5% year over year), Contractors are still aggressively bidding and absorbing the material cost increase to garner more and more work. Developers and Builders are certainly enjoying the bids that are coming in, as pricing is more competitive than it has been in quite a number of years.

The recent concessions by unions, the lack of new development in many suburban areas, and the reduced labor costs of home office staffs are resulting in pricing that is near 2009 levels. This is not to say that pricing will remain at these levels since many of the smaller firms and/or specialty firms have not been able to weather the storm. With fewer firms able to professionally and adequately provide the necessary services, competition is starting to diminish in certain areas.

Even though most construction firms and unions have made substantial concessions to maintain viability during the recession, Developers continue to pressure for lower and lower pricing. As the recovery gains traction, a turnaround may become evident sooner than expected.

Many Clients and Developers agree that we are not over the hump yet, but there are some signs that we are now in the midst of a slow recovery. Did someone say “election year”? Over the next few months we will see whether the recovery is real or just enough improvement to get us past November 2012.

That said, the table below provides mean (average) construction costs of rental apartment construction projects:

| Trade Line Item | Unit Cost | % of Total | Unit |

| Foundation/Pilings | $183.28 | 9.8% | Footprint |

| Superstructure | $28.82 | 15.1% | Total Bldg |

| Exterior Glass | $55.98 | 14.5% | Ext. Glass |

| Exterior Wall | $35.74 | 2.4% | Other Ext. |

| Roofing w/Pavers | $2,220 | 1.2% | Roof Squares |

| Miscellaneous Iron | $0.80 | 0.4% | Total Bldg |

| Interior Partitions | $17.63 | 7.2% | Bldg Equiv |

| Finishes | $14.39 | 6.1% | Bldg Equiv |

| Cabinets & Appliances | $7,494 | 1.4% | Apt. Units |

| Specialties | $8,243 | 1.6% | Apt. Units |

| Elevators | $18,076 | 2.1% | Elev Stops |

| Plumbing | $10.96 | 4.6% | Bldg Equiv |

| HVAC | $20.17 | 8.4% | Bldg Equiv |

| Fire Protection | $3.31 | 1.7% | Total Bldg |

| Electrical | $20.94 | 8.6% | Bldg Equiv |

| General Conditions | 13.0% | 12.5% | % of Total |

| Builder’s Fee | 2.5% | 2.4% | % of Total |

| Building Hard Costs | $237.72 | 100.0% |

When one is comparing project budgets to conventional historical data, there are many aspects of the actual project that require evaluation. Location factors, which are percentage adjustments for particular localities, need to be applied to the mean cost estimates. Construction inflation factors, which are cost adjustments to historical data to reflect the latest labor rates and material cost adjustments for a particular locale must also be applied. Lastly, the level of finish, such as luxury versus moderate income units, will have a significant effect on construction pricing.

Merritt & Harris, Inc. has been providing construction cost analyses for almost 75 years and our industry leading cost reviews are essential to the development process. If you would like to discuss your project or have just general construction cost questions, please contact Mike Dwyer, Principal, at 212.697.3188, ext. 309.

Mexico’s Growing Need for Business-Oriented Hotels

We encourage you to check out this article on current trends in Mexico’s hospitality industry: http://www.hvs.com/article/5328/mexicos-growing-need-for-business-oriented-branded-hotels/

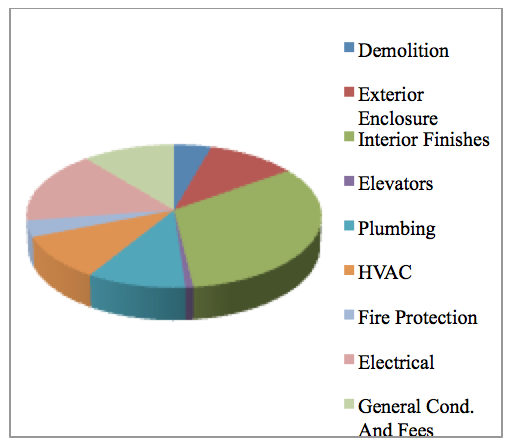

Spring Cost Corner – Office to Residential Conversion

by Mike Dwyer, Principal

Office to Rental Residential

| Trade | Unit Cost | Unt | % of Total |

| Demolition | $3.98 | Total Bldg. SF | 4.4% |

| Exterior Enclosure | $17.53 | Exterior SF | 10.7% |

| Interior Finishes | $32.76 | Bldg. Equiv. SF | 33.0% |

| Elevators | $7,500 | Elevator stops | 0.8% |

| Plumbing | $9.96 | Bldg. Equiv. SF | 10.0% |

| HVAC | $10.07 | Bldg. Equiv. SF | 10.1% |

| Fire Protection | $3.30 | Bldg. Equiv. SF | 3.7% |

| Electrical | $16.23 | Bldg. Equiv. SF | 16.3% |

| General Cond. And Fees | $0.11 | % of Total | 11.0% |

Construction costs are starting to increase primarily due to the cost of materials. Material costs from steel shapes to aluminum and copper are seeing year over year increases of 3.5-9.0%. New commercial construction is starting to see glimmers of hope for a modest recovery, as we said in our last newsletter, but there is still no clear image of the light at the end of the tunnel.

In recent months, we have been engaged to review and monitor a number of conversion projects. Although many traditional workouts are still being classified as “Special Assets”, there are groups of investors and some lenders who are starting to seize the opportunities of low prices to purchase at below market rates and turn the properties into income producers.

While no conversion or renovation can be considered “typical”, and a cost per square foot cannot adequately give a rule of thumb cost for a renovation, the chart included above is based upon an actual project. Unit costs can be gleaned from the chart for such items of work as window replacement, renovated interior finishes, and conversion of mechanical, electrical, and plumbing from residential to office, be wary that the scope of any project must be carefully reviewed to ascertain whether the budget is reasonable. The reference costs are “baseline” costs and must be adjusted for locale.

If you have a specific project you are evaluating and would like a comprehensive cost analysis, please feel free to contact us.

Formula 1 Texas Style

by Tom Richard, AIA, Principal

The United States will finally get its first purpose-built Formula 1 race track. Named “Circuit of the Americas,” the 3.4 mile circuit and its associated architectural and entertainment facilities are beginning to take shape on a 970 acre site in southeast Austin, Texas. After an absence of five years, an official United States Grand Prix will be held at the track in 2012. Formula 1 United States, the race track’s developer, has, in fact, secured the rights to conduct the US Grand Prix until 2021 from the FIA, the sport’s international sanctioning body.

The developer has put together an impressive team. The track itself was designed by Tilke Gmbh & Co, engineers and architects of Aachen, Germany. Tilke is considered to be the world’s pre-eminent racetrack design firm whose modern purpose-built projects include the Bahrain International Circuit, Korean International Circuit, Shanghai International Circuit, Istanbul Park, and others. According to the developer, the Austin design combines “modern features with details reminiscent of the legendary tracks from the ‘60s.” In fact, several of the track’s 20 turns replicate some of racing’s most famous turns from around the world. The natural topography of the Texas hills on which the 3.4 mile track will sit allows for elevation changes of 133 feet.

The racetrack’s facilities have been designed by HKS, a well respected 70-year-old architectural firm whose sports projects include the new Dallas Cowboys Stadium and the MLB Texas Rangers Stadium in Arlington, Texas, and the Lucas Oil Stadium (NFL Colts) in Indianapolis among others. The facilities will include grandstands for 120,000 people placed at strategic locations along the circuit, pit buildings, team suites, restaurants and club suites, several concession buildings, and fan engagement areas. It will truly be a world-class racing facility. The general contractor is Austin Commercial, a major construction firm.

The team behind the project is also first rate. Tavo Hellmund, founding partner and Chairman of Formula 1 United States, was raised in Austin and compiled a winning record as a driver in NASCAR, FIA, and SCCA (Sports Car Club of America) sanctioned races. He is one of the most qualified authorities on Formula 1 racing in the US. The other founding partner of Formula 1 United States is Red McCombs, a co-founder of Clear Channel Communications and former owner of the San Antonio Spurs, Denver Nuggets, and Minnesota Vikings. The President of Formula 1 United States is Steve Sexton, former President and CEO of Churchill Downs and an executive with 25 years of experience in the racing and entertainment business.

Merritt & Harris, Inc. is providing the construction document review and is monitoring the construction of the Circuit of Americas for the lender.